Pioneer in EU Taxonomy

The Dürr Group sees the shift toward greater sustainability as an opportunity. With the Taxonomy Regulation, the European Union (EU) has developed a classification system for environmentally sustainable economic activities, thus creating uniform criteria for companies.

Climate neutral European Union by 2050

With the European Green Deal, the European Union (EU) has set itself the goal of becoming climate neutral by 2050. In order to finance this goal and to make the economic and financial system in the EU more sustainable, capital flows are to be directed toward sustainable investments. To this end, the European Commission has developed the Action Plan on Financing Sustainable Growth. The core element of this action plan is the EU Taxonomy Regulation.

For more information on the EU Taxonomy in the Dürr Group, please refer to our

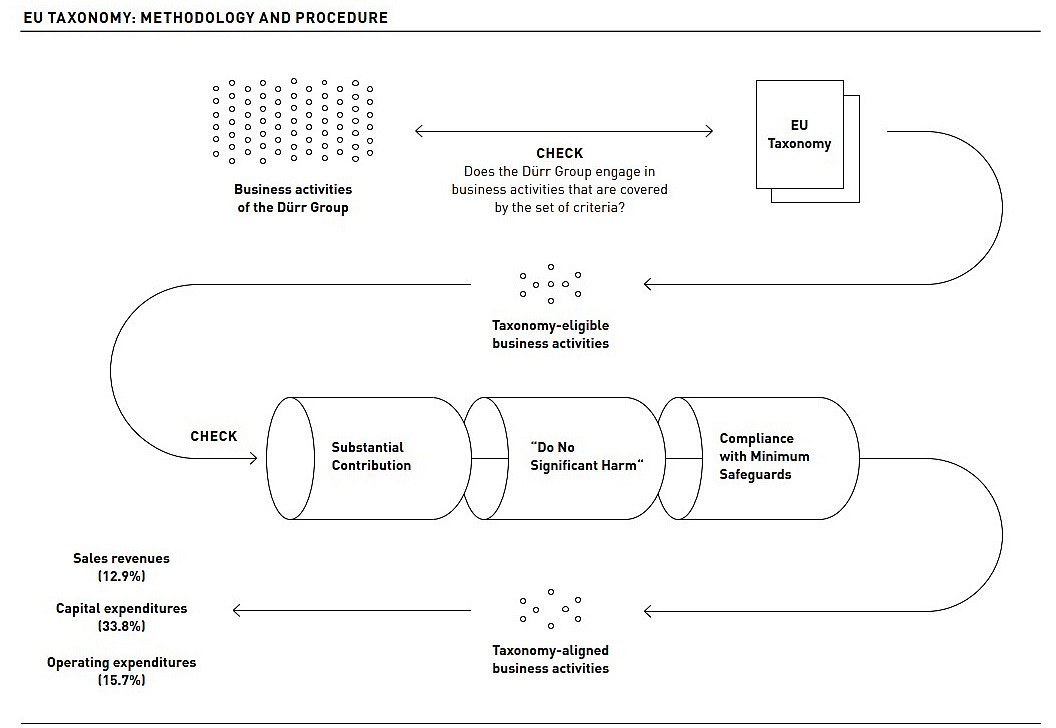

Background and Goals

The core element of the action plan is the EU Taxonomy Regulation. It represents a uniform classification system – a “green list” – for sustainable economic activities. According to the EU Taxonomy Regulation, economic activities are “taxonomy-eligible” if they potentially contribute to the achievement of one of the following six environmental objectives:

1. Climate change mitigation

2. Climate change adaption

3. Sustainable use and protection of water and marine resources

4. Transition to a circular economy

5. Pollution prevention and control

6. Protection and restoration of biodiversity and ecosystems

In addition, economic activities are “environmentally sustainable” or “taxonomy-aligned” according to the taxonomy specifications, if the taxonomy-eligible economic activities

- substantially contribute to the achievement of one or more of the six environmental objectives listed (Substantial Contribution)

- do not significantly harm the achievement of the five other environmental objectives (Do No Significant Harm, DNSH), and

- ensure compliance with minimum safeguards (Minimum Safeguards).

Implementation of the Taxonomy requirements

Assignment of economic activities to relevant taxonomy criteria

The following economic activities defined by the EU Taxonomy have been identified for the recognition and assignment of the Dürr Group’s sales revenues, CapEx, and OpEx to the first environmental objective “climate change mitigation”:

- 3.1 Manufacture of renewable energy technologies

- 3.6 Manufacture of other low carbon technologies

- 4.11 Storage of thermal energy

For the 2024 fiscal year, further economic activities have been identified for the recognition and assignment of taxonomy-eligible CapEx and OpEx of the Dürr Group for the first environmental objective “climate change mitigation”:

- 6.5 Transport by motorbikes, passenger cars, and light commercial vehicles

- 7.3 Installation, maintenance and repair of energy efficiency equipment

- 7.6 Installation, maintenance and repair of renewable energy technologies

- 7.7 Acquisition and ownership of buildings

Three prerequisites for environmentally sustainable economic activities

1. Substantial Contribution

Compliance with the criteria for a substantial contribution to the first environmental objective, “climate change mitigation,” which is relevant to the Dürr Group, was assessed individually for each taxonomy-eligible business activity of the Dürr Group. In the analyses conducted, no economic activity was identified that makes a substantial contribution to the remaining five environmental objectives.

For the 2023 fiscal year, the following business activities of the Dürr Group have been identified for the recognition and assignment of taxonomy-eligible sales revenues, CapEx, and OpEx.

2. Avoidance of significant harm

Furthermore, we analyzed whether the achievement of the five remaining EU environmental objectives is significantly harmed by the business activities listed above. For this purpose, it was appropriate to regularly assess DNSH compliance at the level of the business activities and at the level of the Dürr Group’s locations. The locations assessed as relevant were those which accounted for significant value-adding processes for taxonomy-eligible business activities or environmentally sustainable CapEx and OpEx in the 2024 fiscal year. Subsequently, a comparison was made with the DNSH criteria for the selected locations.

As a result, we have not identified any significant harm to the achievement of the five other environmental objectives at any relevant location. For further information, please refer to our → Sustainability Statement 2024.

3. Compliance with Minimum Safeguards

The Dürr Group is committed to respecting human rights and promoting fair working conditions. This applies in particular to dealings with its own employees and direct suppliers. Our actions are guided by the OECD Guidelines for Multinational Enterprises, the United Nations Guiding Principles on Business and Human Rights (UNGP), and the Core Labor Standards of the International Labour Organization (ILO), among others. In the 2024 fiscal year, we again reviewed compliance with these guiding principles and standards in our business activities across the Group, focusing on the following areas: respect for human and employee rights, combating bribery and corruption, taxation, and (fair) competition.

The result showed that our Group-wide processes and systems are suited to reliably identify potential risks or violations at our locations worldwide.

Performance indicators according to the EU Taxonomy Regulation

In the following, we provide information on our Group-wide taxonomy-eligible and taxonomy-aligned sales revenues, CapEx, and OpEx in accordance with the EU Taxonomy for the 2023 and 2024 fiscal years. Taking into account the technical screening criteria, it is possible that taxonomy-eligible and taxonomy-aligned sales revenues and CapEx differ in their results. Taxonomy-eligible and taxonomy-aligned OpEx of the Dürr Group, on the other hand, regularly correspond to each other.

| Taxonomy-eligible share 2024 (%) | Taxonomy-aligned share 2024 (%) | Taxonomy-eligible share 2023 (%) | Taxonomy-aligned share 2023 (%) | |

|---|---|---|---|---|

| Sales revenues | 15.8 | 12.9 | 18.41 | 16.11 |

| CapEx | 52.0 | 33.8 | 35.0 | 13.4 |

| OpEx | 15.7 | 15.7 | 11.51 | 11.51 |

1 As reported in 2023, including the discontinued operation (environmental technology business).

Sales revenues

In the 2024 fiscal year, the Dürr Group’s taxonomy-aligned sales revenues amounted to €552.1 million. This represents a year-on-year decrease of 25.9% (previous year: €744.8 million). The background to this is that the environmental technology business will be classified as a discontinued operation in the 2024 consolidated financial statements. For this reason, the sales revenues allocated to the environmental technology business under business activity “4.11 Storage of thermal energy” and business activity “3.1 Manufacture of renewable energy technologies” will not be reported in the 2024 fiscal year.

On a comparable basis, i.e. adjusted for the sales generated by the discontinued operation in the 2023 fiscal year, this results in an increase in taxonomy-eligible sales revenues of 8.9% to €679.7 million for 2024 (previous year €624.2 million). On this basis, taxonomy-aligned sales revenues increased by 6.4% year-on-year to €552.1 million (previous year: €518.8 million). This resulted from an increase in activities in the context of economic activity “3.6 Manufacture of other low carbon technologies,” where the Dürr Group recorded a significant increase in demand in the areas of electromobility and battery manufacturing technology. The share of taxonomy-eligible sales revenues increased to 15.8% in the 2024 fiscal year (previous year: 14.9%). The share of taxonomy-aligned sales revenues rose to 12.9% (previous year: 12.4%).

CapEx

Taxonomy-eligible CapEx including the CapEx of the discontinued operation amounted to €98.2 million in the 2024 fiscal year (previous year: €123.4 million). Of this, €63.8 million (previous year: €47.2 million) met the criteria of the EU Taxonomy Regulation for taxonomy-aligned CapEx. The increase is primarily due to investments in new buildings at BENZ in Gengenbach and at HOMAG in Środa Wielkopolska (Poland), which are assigned to economic activity “7.7 Acquisition and ownership of buildings.” In addition, capitalized development costs in the areas of battery production technology and painting technology as well as investments in the solid-wood manufacturing sector caused an increase in environmentally sustainable CapEx in the context of economic activity “3.6 Manufacture of other low carbon technologies.”

The difference between taxonomy-eligible and taxonomy-aligned capital expenditures in the amount of €34.4 million resulted from investments assigned to economic activities “6.5 Transport by motorbikes, passenger cars, and light commercial vehicles” and “7.7 Acquisition and ownership of buildings,” though it was not possible to demonstrate a substantial contribution to the first environmental objective “climate change mitigation” in all cases. In the 2024 fiscal year, 33.8% of our investments complied with the requirements of the EU Taxonomy Regulation for taxonomy-aligned CapEx (previous year: 13.4%). The increase in percentage terms compared to the previous year is due to the one-off effect from acquisitions in 2023. The taxonomy-aligned share of investments in non-current intangible assets amounted to 10%, while tangible assets accounted for 90%.

OpEx

As in the previous year, the Dürr Group’s taxonomy-eligible OpEx corresponded to taxonomy-aligned OpEx, amounting to €22.0 million (previous year: €16.5 million including OpEx from the discontinued operation).

On a comparable basis, i.e. adjusted for the OpEx from the discontinued operation for the 2023 fiscal year, this results in an increase of €6.5 million compared to the previous year (previous year: €15.5 million). The taxonomy-eligible or taxonomy-aligned share of the Dürr Group’s relevant OpEx in accordance with the Taxonomy Regulation amounted to 15.7% in the year under review (previous year: 11.0%) according to this consideration. One important component was non-capitalizable expenses for research and development, particularly in the areas of battery production technology, the filling of battery cells, and solid-wood manufacturing. These expenses contributed 94% to the taxonomy-eligible or taxonomy-aligned OpEx (previous year: 87%).

Economic activity 3.6 „Manufacture of other low carbon technologies“

The activity description “3.6 Manufacture of other low carbon technologies” is of particular relevance to the Dürr Group. Due to the generic description of this economic activity, it is necessary to describe our interpretation in greater detail. The economic activity includes activities for the production of technologies that aim at substantial reductions in greenhouse gas emissions in other sectors of the economy. From the Dürr Group’s perspective, a substantial reduction means a decrease in greenhouse gas emissions in the use phase by at least 20%. Such a substantial reduction can usually only be achieved by a technological leap and not by continuous improvements. We have therefore set the value of 20% as the minimum level for a substantial reduction in greenhouse gas emissions.

Furthermore, the technical screening criteria for economic activity 3.6 describe requirements for the quantification of life-cycle greenhouse gas emissions. We commissioned the Fraunhofer Institute for Building Physics (IBP) to prepare science-based lifecycle greenhouse gas balances for representative machines and systems. In assessing the lifecycle emissions of goods manufactured with our machines and systems, we relied on published data and analyses from recognized scientific organizations.